HealthManagement, Volume 18 - Issue 3, 2018

PRINT OPTIMISED

PRINT OPTIMISED

Effective implementation of Ayushman Bharat - India’s National Health Protection Mission (AB-NHPM) will largely depend on ensuring that the package of services prioritised under the National Health Protection Scheme is based on community needs, evidence-based, well governed and inclusive.

There is arguably no aspect of social policy more complex or controversial in today’s world than how a country goes about assuring health for its people. Major challenges facing the Indian public healthcare system are the sheer complexity of financing and managing preventive, promotive, curative and rehabilitative care; of proactively addressing the social determinants of health; of assuring quality in the public sector; of harnessing the initiative and resources of the private sector while ensuring effective regulatory systems; and of ensuring equity of access to services across social and economic divides.

Since the Union Budget 2018 announcement on the Ayushman Bharat-National Health Protection Mission (AB-NHPM), valuable viewpoints, evidence and analysis have come up containing a mix of admiration and scepticism. As a result, the NHPM has been labelled many things—visionary, populist, pro-private insurance market, scaled-up version of old schemes, pre-election gimmick and more. The most important question that remains in the minds of health economists is how will publicly funded health insurance cover a population ten times that of Obamacare with less than a hundredth of a budget and still reduce out-of-pocket expenditure of patients.

Current status of health financing including health insurance in India

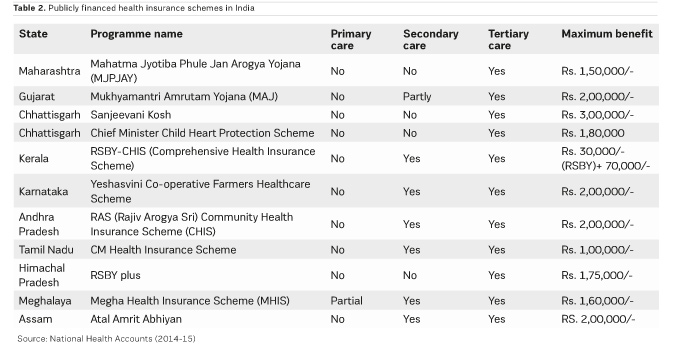

Public health expenditure in India (total of central and state governments) remained constant at approximately 1.3% of gross domestic product (GDP) between 2008 and 2015 and increased marginally to 1.4% in 2016-17. Including the private sector, total health expenditure as a percentage of GDP is estimated at 3.9%. In 2018-19, the Ministry of Health and Family Welfare received an allocation of Rs. 54,600 crore. The National Health Mission received the highest allocation at Rs.30,130 crore and constituted 55% of the total allocation. According to the National Family Health Survey 4 (2015-16) (Ministry of Health and Family Welfare 2017), only 29% of households in India have one member covered under any health insurance scheme, be it public or private (20% women and 23% men). The top five states according to coverage are Andhra Pradesh (75%), Chhattisgarh (69%), Telangana (66%), Tamil Nadu (64%) and Tripura (58%).

You might also like: Making Affordable Healthcare Profitable

In-patient hospitalisation expenditure in India has increased nearly 300% during the last ten years (National Sample Survey Office 2015). Household health expenditures include out-of-pocket expenditures (OOPE) (95%) and insurance (5%). According to the National Health Accounts (2014-15), total OOPE is 3.02 lakh crore. The highest OOPE is made towards purchasing medicines—1.30 lakh crores. (43%), followed by private hospitals—86,189 crores (28%).

OOPE is typically financed by household revenues (71%). Rural households primarily depended on their 'household income/savings' (68%) and on 'borrowings' (25%) while urban households relied much more on their 'income/saving' (75%) for financing expenditure on hospitalisations and on (18%) borrowings (National Sample Survey Office 2015). OOPE in India is over 60%, which leads to nearly 6 million families getting into poverty due to catastrophic health expenditures.

AB-NHPM salient features

- There

are basically two pillars of AB-NHPM. One is the strengthening of primary

healthcare by converting sub-centres into Health and Wellness Centres and

second is the National Health Protection Scheme (NHPS) for the vulnerable 40%

of the Indian population (10.74 crore families) based on the Socio-Economic

Caste Census database.

- NHPS

will have a defined benefit cover of Rs.5 lakh per family per year covering

1,347 treatments. The beneficiaries can avail benefits in both public and

empanelled private hospitals. AB-NHPM will subsume the ongoing centrally

sponsored health insurance schemes- Rashtriya Swasthya Bima Yojana (RSBY) and

the Senior Citizen Health Insurance Scheme.

- Total

expenditure will depend on actual market-determined premium paid in

States/Union Territories (UTs) where AB-NHPM will be implemented through

insurance companies. In States/UTs where the scheme will be implemented in

Trust/Society mode, the central share of funds will be provided based on actual

expenditure or premium ceiling (whichever is lower) in the predetermined ratio.

AB-NHPM objectives

- Reduce

out-of-pocket expenditure (OOPE)

- Increase

access to quality health and medications

Institutional structure

The Government of India will set up three bodies:

1. National Health Protection Mission Council

Function: provide policy guidance to AB-NHPM.

Composition: co-chaired by Union Health and Family Welfare Minister and Vice-Chairman of National Institution for Transforming India (NITI Aayog).

Members: health ministers of all States/UTs.

2. Ayushman

Bharat National Health Protection Mission Governing Board

Function: decision-making body.

Composition: jointly chaired by Secretary (Health and Family Welfare) and Member (Health), NITI Aayog with Financial Advisor, Ministry of Health and Family Welfare (MoHFW), Additional Secretary & Mission Director, Ayushman Bharat National Health Protection Mission, MoHFW (AB-NHPM) and Joint Secretary (AB-NHPM), MoHFW as members.

3. Ayushman Bharat - National Health Protection Mission Agency (AB-NHPMA)

Composition: headed by full-time CEO at the level of Secretary/Additional Secretary to the Government of India.

Function: to manage the AB-NHPM at the operational level in the form of a Society.

4. State Health Agency (SHA)

These will be created in every state of India to implement the scheme. States/UTs can decide to implement the scheme through an insurance company or through a trust.

Six different working groups on processes, information technology, fraud detection and grievances, awareness generation, institutional arrangement and continuum of care were formed in the first meeting of NITI Aayog with MoHFW and State Health secretaries.

Health and wellness centres

Cost-effective health coverage must cover primary care. This is where the second feature of Ayushman Bharat Programme—the creation of 150,000 health and wellness centres across the country—is very significant. The previous government missed the bus when it failed to implement the recommendations of the High-Level Expert Group (HLEG) on Universal Health Coverage (UHC) (Planning Commission of India 2011). However, those recommendations resonate in the National Health Policy 2017, NITI Aayog’s three-year action agenda (2017-2020) and Union Budget of 2018 when they mention “Assuring availability of free, comprehensive primary health care services” at sub-centre level. Sub-centres are the first line of contact of citizens to the public health system in India. Yet, even with the talk about strengthening health at the grassroots, overall allocation to the Department of Health and Family Welfare rose by a meagre Rs. 1,250 crore from the revised Budget estimate for 2017-2018, and allocations to the National Health Mission have fallen by more than Rs.600 crore. Our biggest constraint is also an acute shortage of human resources.

Learnings from Rashtriya Swasthya Bima Yojana (RSBY)

RSBY was announced by Prime Minister Manmohan Singh in August 2007. The aim of the scheme was to “improve access of below the poverty line (BPL) families to quality medical care for treatment of diseases involving hospitalisation and surgery through an identified network of healthcare providers” (Rashtriya Swasthya Bima Yojana 2009). The scheme provided for annual coverage of up to Rs. 30,000 per household. The policy covered hospitalisation, daycare treatment and related tests, consultations and medicines as well as pre- and post-hospitalisation expenses for some 700 medical and surgical conditions and procedures. During 2016-2017, 3.63 crore families were covered under RSBY in 278 districts of the country, and they could access medical treatment across the network of 8,697 empanelled hospitals.

The Situation Analysis document of National Health Policy 2017 mentioned concerns regarding RSBY: “Low awareness among the beneficiaries about the entitlements and on how and when to use the RSBY card. Another concern is related to denial of services by private hospitals for many categories of illnesses and oversupply of some services. Some hospitals, insurance companies and administrators have also resorted to various fraudulent measures, including charging informal payments” (Gupta 2017). Additionally, it notes: “Schemes that are governed and managed by independent bodies have performed better than other schemes that are located in informal cells within existing departments or when managed by insurance companies” (Gupta 2017).

NHPS is different from RSBY in one fundamental way: RSBY was based on enrolment whereas NHPS is an entitlement-based scheme, ie all the identified population sub-groups under NHPS will automatically get covered once the scheme becomes operational. The functions of risk and resource pooling, which is the central role of any insurance company, are almost non-existent in NHPS as the scheme is fully subsidised by the Central and State Government through their budgetary support. The key functions that remain central in NHPS are hospital empanelment and claims settlement.

RSBY provided limited coverage of only Rs. 30,000, usually for secondary care. Though it improved access to healthcare, it did not significantly reduce OOPE as proved in many studies. The NHPS tries to address those concerns by sharply raising the coverage cap, but shares with the RSBY the weakness of not covering outpatient care. which accounts for the largest proportion of OOPE.

“We will give specific QR codes to families entitled to the scheme. QR code or a barcode is a machine-readable optical label that will contain information about the families and their members. These codes will be sent to the beneficiaries’ addresses. Learning from RSBY we decided not to issue cards, for saving time as it took more than one year to distribute cards in RSBY,” said Preeti Sudan, secretary, Ministry of Health and Family Welfare (Sharma 2018).

Challenges in effective implementation of NHPS

As the National Health Policy 2017 concludes: “A policy is only as good as its implementation” (Sundararaman 2017). Selecting the insurance provider is an extremely complex process. Each step, such as the design of the tender documents, contract and legal agreements, payment terms, penalties for non-compliance, pre-qualification of bidders, transparent and secured e-tendering process, which tenders would be called state-wise or nationally—must be considered carefully. Otherwise, the process would invite unnecessary litigation.

I discuss below the advantages and disadvantages of both the models: Trust and insurance.

Trust model

Key advantages of implementing the scheme through a trust model are:

- its not-for-profit

orientation

- conducting awareness and

sensitisation functions using government administrative machinery, especially

at district/sub-district level.

Risks of this model are:

- weak in-house capacity

to perform critical functions that depend on the quality of hired personnel

(having requisite skills and competencies)

- a weak governance

structure that fails to achieve professional conduct and to prevent outside

interference. Andhra Pradesh, Telangana, Karnataka and Gujarat are using the

trust model.

Insurance model

Some of the main advantages of implementing the scheme through an insurance company are:

- its experience of

working with third-party administrators (TPAs)

- possible scale-up of

scheme to cover the non-poor population, which would involve marketing of the

scheme and premium collection

- better deployment of

short-term surpluses to generate better returns on those surpluses.

The risk associated with this model though is in cost-escalation overtime through possible collusion between for-profit entities (insurers, TPAs, and healthcare providers). Maharashtra and Tamil Nadu are currently using the insurance model.

Conclusion

In conclusion, I would like to quote Anil Swarup, Secretary, Ministry of Human Resource Development, “An idea is worth its salt if it is politically acceptable, socially desirable, technologically feasible, financially viable and administratively doable” (Swarup 2017).

In a federal polity with multiple political parties sharing governance, although the Bharatiya Janata Party is currently the ruling party in 21 states, an all-India consensus on the design and implementation of NHPS requires a high level of cooperative federalism, both to make the scheme viable and to ensure portability of coverage across states.

Overall, the effective implementation of AB-NHPM will largely depend on ensuring that the package of services prioritised under NHPS is based on community needs, evidence-based, well governed and inclusive.

As the Government of India has made districts a geographical unit of policymaking through its aspirational districts programme, my recommendations are:

- Coordination

between multiple stakeholders entrusted with the implementation of NHPS needs

to be 100 percent. A study conducted in Karnataka (Rajeshkar et al. 2011)

showed that the level of organisation was much greater in districts where the

district collector took an active interest in implementation and monitoring of

RSBY. Every district collector should include AB-NHPM in its monthly review

meeting by focusing on access and coverage to the last mile and significant

improvement in health outcomes from the last National Family Health Survey

(NFHS) (2015-16) (Ministry of Health and Family Welfare 2017).

- Implementation needs to be accompanied by analysis so that the solutions are found through policy analysis and research embedded into implementation. This calls for strengthening “evidence-to-policy” links.

References:

Government of India. Press Information Bureau (2018) Cabinet approves Ayushman Bharat – National Health Protection Mission. 21 Mar. Available from pib.nic.in/newsite/PrintRelease.aspx?relid=177816

Gupta RP (2017) National health policy 2017: situational analysis. Available from slideshare.net/rajendrapgupta/national-health-policy-2017-situational-analysis

Kinnan C, Malani A (2018) Roadmap for a successful Modicare. Livemint 6 Mar. Available from livemint.com/Opinion/enERYnZY3MVuxvCzMpEuiJ/Road-map-for-a-successful-Modicare.html

Ministry of Health and Family Welfare (2017) National Family Health Survey (NFHS-4): 2015-16. Mumbai: International Institute for Population Sciences. Available from indiaenvironmentportal.org.in/files/file/India_2.pdf

Nagar D (2018) Will Modicare or NHPS Bridge the Healthcare Gap for India? BW Disrupt 9 Apr. Available from bwdisrupt.businessworld.in/article/Will-Modicare-or-NHPS-Bridge-the-Healthcare-Gap-for-India-/09-04-2018-145848

Narayanan N (2018) Interview: ‘Insurance should not be the only financing model for public healthcare in India’. Scroll.in 17 Feb. Available from scroll.in/pulse/869000/interview-insurance-should-not-be-the-only-financing-model-for-public-healthcare-in-india

Paul V, Shukla A, Sundararaman T (2018) Can Ayushman Bharat make for a healthier India? The Hindu 13 Apr. Available from

thehindu.com/opinion/op-ed/can-ayushman-bharat-make-for-a-healthier-india/article23516837.ecePlanning Commission of India (2011) High Level Expert Group Report on Universal Health Coverage for India. Available from planningcommission.nic.in/reports/genrep/rep_uhc0812.pdf

Rajeshkar D et al. (2011) Implementing health insurance: the rollout of Rashtriya Swasthya Bima Yojana in Karnataka. Economic & Political Weekly XLVI (20): 56-63.

Ranganathan S (2018) NHPS remains strategy on paper unless delivery machinery overhauled. Livemint 7 Apr. Available from livemint.com/Opinion/pjI5wFA6jmf7RmOpAA0b2I/NHPS-remains-strategy-on-paper-unless-delivery-machinery-ove.html

Rao N (2018) India’s health protection scheme does little to address biggest cost to patients – buying medicines. Scroll.in, 11 Apr. Available fromscroll.in/pulse/875017/indias-health-protection-scheme-does-little-to-address-biggest-cost-to-patients-buying-medicines

Rao SK (2017) Do we care: India’s health system. New Delhi: Oxford University Press.

Rao SK (2018) Is India ready for NHPS? The Indian Express 13 Feb. Available from indianexpress.com/article/opinion/columns/national-health-schemes-budget-2018-primary-healthcare-hospitals-is-india-ready-for-nhps-5061319

Rashtriya Swasthya Bima Yojana (2009) Tender document - template for use by state governments. Available from rsby.gov.in

Ravi S, Sood N (2018) Is the National Health Protection Scheme good public policy? Livemint 12 Mar. Available from livemint.com/Opinion/3GqDnEIYPxbuzwJuT4dkaM/Is-the-National-Health-Protection-Scheme-good-public-policy.html

Reddy KS (2018) Making health insurance work. The Hindu 6 Feb. Available from thehindu.com/opinion/op-ed/making-health-insurance-work/article22661666.ece

Reddy KS (2018) National Health Protection Scheme: why insurance can’t replace primary healthcare. Financial Express, 9 Feb. Available from financialexpress.com/opinion/national-health-protection-scheme-why-insurance-cant-replace-primary-healthcare/1058904

Reddy KS et al. (2011) A critical assessment of the existing health insurance models in India. New Delhi: Public Health Foundation of India. Available from planningcommission.nic.in/reports/sereport/ser/ser_heal1305.pdf

Selvaraj S, Karan AK (2012) Why publicly-financed health insurance schemes are ineffective in providing financial risk protection. Economic and Political Weekly 47: 60-68.

Sharma NC (2018) Modicare gets Rs10,000 crore allocation, to be fully functional by October. Livemint 23 Mar. Available from livemint.com/Politics/GIHy0byz4oisZe4W2RckDN/Modicare-gets-Rs10000-crore-allocation-to-be-fully-functio.html

Sundararaman T (2017) National Health Policy 2017: The challenges of implementation. DNA 28 Mar. Available from dnaindia.com/analysis/column-national-health-policy-2017-the-challenges-of-implementation-2371059

Sundararaman T (2018) How Thailand built a universal healthcare system without giving private sector free rein. Scroll.in, 20 Feb. Available from scroll.in/pulse/869171/thailand-built-a-universal-healthcare-system-without-giving-private-sector-free-rein

Sundararaman T (2018) In new health and wellness centres, India has a good plan for primary care – backed by little action. Scroll.in, 1 Mar. Available from scroll.in/pulse/870405/in-new-health-and-wellness-centres-india-has-a-good-plan-for-primary-care-backed-by-little-action

Sundararaman T (2018) Lessons from Thailand: for universal health coverage, invest in public systems and human resources. Scroll.in, 19 Feb. Available from scroll.in/pulse/869170/lessons-from-thailand-for-universal-health-coverage-invest-in-public-systems-and-human-resources

Swarup A (2017) Nonprofits don’t need to scale dramatically. India Development Review 28 Jun. Available from idronline.org/nonprofits-dont-need-to-scale-dramatically