HealthManagement, Volume 12 - Issue 2-3, 2012

Author:

Prof. Bernd MayBoth managers in the medical imaging department (MID), as well as hospital managers, are seeking new ways to provide an optimised service within a climate of shrinking healthcare budgets, competition from private imaging centres, and increased demand for evidence- based medical provision. In this article, I will outline four key ways in which the MID can attain these goals, and demonstrate through a comparision of the performance, cost-effectiveness and management of several types of medical imaging facilities, that there is much work to be done to remain competitive. The following are key factors for optimised cost management:

- Select approriate exams to reduce length of hospital stays;

- Recognise that labour is one of the key cost drivers in the department;

- Hospital managers must realise the impact of the high costs of running and maintaining equipment; and

- All types of medical imaging facilities would benefit by considering a public-private cooperation for provision of imaging services.

Selecting Appropriate Exams

Financial management in the MID in a diagnosis related group (DRG)-driven hospital can be assessed by looking at both revenue and cost. Revenues are generated, for example, from diagnostic services provided to outpatients as well as from treatments provided in interventional radiology, based on specific DRGs. Costs are strongly tied to the diagnostic function and effectiveness of an MID. However, as there are no specific DRGs allocated for diagnostic service provision in our present system, costs are being charged to the referring departments according to the amount and structure of utilisation (fee-per-service, e.g. an ultrasound ~ 60-70 euros, conventional x-ray ~ 50-60 euros, CT ~ 100-160 euros, MRT ~ 200-400 euros, depending on the specifications of modality, average daily load and staffing).

In an ideal world, the diagnostician would stream the patient’s pathway, as follows:

- Respond to the requirement of any referring department on demand;

- Verify the indication for referral by trained diagnosticians;

- Control the diagnostic pathway in the MID using trained radiologists;

- Employ an imaging procedure that delivers adequate sensitivity and specificity;

- Avoid any diagnostic sequences with various modalities (same or different); and

- Make findings available in the referring department the same day (≤ 3 hours after exam).

These criteria are all about optimising the financial and budget management issues of any MID. However, these are merely ideals. In the real world, there are two major financial issues to be defined: the total running costs of diagnostic service and the outcome of inpatient care per DRG. Nevertheless, we can clearly see that the provision of inpatient care has a significant overall financial impact on medical imaging.

Reducing Length of Stay by Streamlining Exam Selection

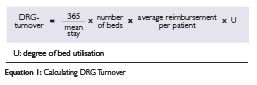

Our analysis shows that the total costs of the medical imaging department range from about 4–7 percent (on average 5 percent) of overall DRG turnover in the hospital. The cost saving potential amounts to about 20 percent of total cost of the MID, i.e. about one percent of DRG turnover of the hospital. We examined data from our radiology information system (RIS) to estimate the financial impact of inpatient imaging services, and found that on average, between 50 and 90 percent (with a mean of 75 percent) of all inpatients receive medical imaging services during their hospital stay, of which about two thirds are referred for multiple diagnostic services either with the same or a different modality, i.e. 50 percent of all inpatients are being diagnosed by means of at least two modalities resulting in at least 1.5 days of an extension of their stay in hospital. To estimate the cost impact of these multiple imaging exams, we must take a look into the relationship between DRG turnover, mean stay, number of beds per hospital and average reimbursement per inpatient (Equation 1):

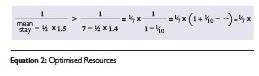

The most significant factor we should look at to drive down costs is the mean stay, which is about seven days per inpatient. We can reduce costs by ensuring that the first diagnostic exam prescribed is the optimal one, avoiding a spiral into further tests which prolongs hospital stays and wastes resources. This could potentially reduce the mean stay by 1.5 days for 50 percent of all inpatients, which can be shown by altering the equation (Equation 2).

This formula proves that the abovementioned outcome of better referrals and wiser exam choices, avoids a diagnostic domino effect and can optimise the total turnover of the hospital by 10 percent. This strategy of avoiding unnecessary exams for all inpatients in the hospital, most of whom will require some sort of diagnostic imaging exam at some point in their stay, clearly supports a quality foundation for the management of medical imaging services.

Do Oncologic and Trauma Patients Really Need Multiple Exams?

One argument presented by the directors of medical imaging to the above cost management method is their belief that the majority of inpatients suffer from either oncological or trauma-related diseases, which require multiple diagnostic exams before and after treatment. From the analysis of RIS data from many large- and medium-sized hospitals as well as university clinics, we have been seeing a different result, as oncological and trauma patients in particular are experiencing highly redundant diagnostic exam pathways of the same organ with different modalities, which easily can be reduced by at least a factor of two if proper case management is applied.

We concede that the analysis of clinical and diagnostic pathways and the discussion of the results with clinicians and diagnosticians will always be a challenging task to fulfill, but it is worth doing, since it is beneficial for the quality of service for patients as well as the performance and revenue of the hospital.

Hospital Managers and Imaging Costs

The majority of hospital managers concentrate their efforts on controlling the direct costs of the MID, which only has a maximum financial impact of up to one percent of DRG turnover. About 80 percent of the total running costs of any MID consist of both labour costs, accounting for up to 60 percent, with costs of equipment (depreciation and interest of financing modalities, running costs for customer service, etc.) accounting for the remaining 20 percent. Hospital managers would be better placed if they would turn their attention to labour and equipment financing and maintenance as significant cost drivers for medical imaging.

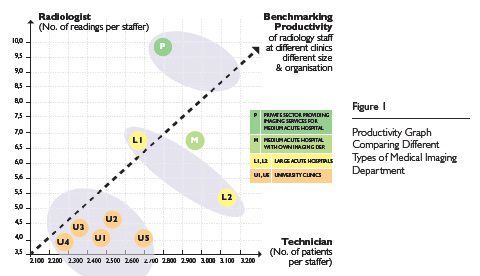

To get to an estimate of the cost saving potential of focusing on labour costs, we recommend using a benchmarking tool. The primary benchmark is the productivity of medical staff (radiologists and technicians, see Figure 1). The overall costs of labour are divided into about 75 percent going towards medical staff cost and the remaining 25 percent being allocated to administrative staff (in a DRG environment, the cost of medical staff accounts for 90 percent of costs for CT and MRI, about 33 percent of costs for con-ventional x-ray and approximately 25 percent for ultrasound).

The productivity graph allows you to discriminate the productivity of the MID between four groups of hospital:

• University clinics (UC);

• Large acute hospitals (LAH);

• Medium acute hospitals (MAH); and

• MAHs that work with a private imaging practice (P). These tend to be the best financial performers of each of the four in this group, followed by MAH, LAH and finally the university clinics.

University clinics, being burdened by the heavy costs of teaching, educating and training young academics, have traditionally meant reduced productivity and increased labour costs. However, one way in which university clinics are addressing this sluggish performance is by separating research as an entity from the management of inpatient care, which means that the productivity of physicians can be increased (see U2 on the productivity graph). From the productivity graph you can easily see one important result at first glance, which is that the ratio of maximum and minimum productivity of radiologists is about 2.5 whereas the same ratio of technicians is about 1.4. The radiologists in the private imaging practices (marked‚ P in the graph) are the best performers in terms of productivity.

For the group labelled L2, large acute hospitals, the productivity is accounted for as CT technicians were receiving an incentive for increasing their productivity (in this case, a very high case load of 12,000 patients between 8.00 a.m. and 5.00 p.m. on one CT). The performance of the technicians in the medium acute hospital (here, labelled, M) was the result of a low number of MRIs being performed in favour of a high percentage of conventional x-rays (a case cycle for MRI of about 30 to 40 minutes and for conventional x-ray of about 10 minutes).

Modalities that Require High Staff Numbers Drive Costs

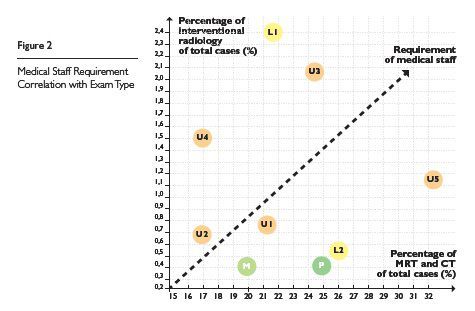

Managing an imaging department in the face of financial restrictions requires looking into those exams which require a higher number of medical staff (see Figure 2). Interestingly, in our graphs you can see that a large acute hospital (L1) is on the same level as two high-end university clinics (U3, U5), whereas the productivity of the L1 staff is better than all of the university clinics. This indicates a dedicated workflow management process is the key factor for success. Interventional radiology and particularly MRI are fast-growing areas within MID, requiring more medical staff than conventional x-ray.

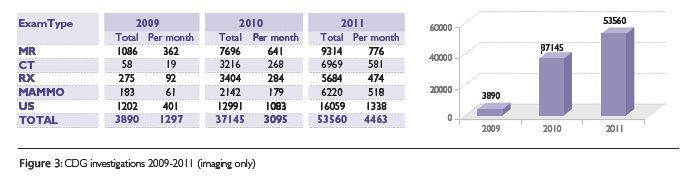

Another important indicator for medical staff is the correlation with complexity of diagnostic effort, measured by the average number of investigations per patient and the number of readings per investigation, the first one correlating with the number of times a patient is visiting a modality (technician), the second one with the number of organs per investigation to be analysed and read by a diagnostician (see Figure 3). If the management of the MID adheres to the quality criteria 2, 3 and 4 in the early part of this paper, the complexity of diagnostic efforts will be significantly reduced, consequently impacting labour cost. Budgeting for labour costs need not necessarily mean neglecting the quality of services provided, it simply means that a logical approach to streamlining treatment pathways and making sensible, evidence-based choices of imaging exams will tie in with an overall approach to cost management.

Another way of benchmarking cost issues is to take account of innovations of modalities which are improving specific productivity, and finally proper IT to support an efficient workflow (RIS/PACS, networked with KIS) and overall approach to cost management.

Consider a Public-Private Cooperation

We briefly discuss the issue of gaining additional revenues with MID from serving outpatients. The most rewarding and selfsustaining approach is being represented by the group labelled P (Figure 1), in which a private practice cooperates with a hospital to provide imaging and interventional radiology services to its inpatients. To consolidate such a cooperation financially, organisationally and economically, it is recommended to set up a legal body shared by both parties. This approach is applicable to all types of imaging facilities, even large acute hospitals and university clinics. The organisation of such a cooperation aims at leaving inpatient and outpatient care with the private practice and financial controlling with the hospital. Radiologists in the private practice are thusly incentivised and rewarded for their high productivity. This type of contracting of inpatient care is based on a pay-per-exam model. Generally, a hospital will save at least 20 percent of the total running cost of its MID before the cooperation and get additional revenue from the earnings per share.

In addition, this kind of cooperation leaves the door open for an expanded collaboration in which the private practice can use their clinical strengths to serve outpatients (e.g. non-invasive cardio-imaging, interventional radiology, onco-imaging, paediatric imaging, etc) and generate additional DRG turnover for the hospital. In some of these cases, patients will need inpatient care in a further step which generates increased DRG turnover.

The imaging department in the context of a public-private cooperation would be well placed to run on a much lower cost basis, as it benefits from a much better utilisation of the most expensive resources (labour, equipment, etc.).

A shareholder structure in this framework gives the hospital management the strategic power to plough entrepeneural and medical resources into the imaging department, further strengthening it. Through this strategy, even the financing of innovations would be better placed, as young academics are receiving training in workflow management which builds their job prospects and the reputation of the medical centre. This creates a triple win-win situation, for the hospital, private practitioners and, last but not least, the patients.

In Conclusion

our studies, represented by the graphs provided, clearly show that clinical imaging within the MID is not always operated or managed in the best way. Without wishing to commoditise our profession, medical imaging cannot ignore modern business strategies and hope to remain competitive with private enterprises, particularly in this challening financial climate of shrinking healthcare budgets. We must do our utmost to maximise revenue and manage our operating costs, while continuing to provide a high level of service to patients and referrers. I hope that within this paper, you have found some suggestions for new ways to manage the business of diagnosing and treating patients.